Executive summary

The shift to digital commerce is creating profound changes for merchants as they develop ways to meet the rapidly evolving demands and preferences of consumers. Electronic payment providers can help merchants deal with the complexity of digital payments — and ultimately increase customer loyalty and engagement — but only if the two entities collaborate effectively, particularly regarding the use of data.

The Strategy& 2015 Consumer Payments Survey, conducted with the Electronic Transactions Association, looks at the implications of the shift to digital commerce for both merchants and payment providers. Among other findings, the results indicate that merchants seek more value-added services from payment providers, which are still largely focused on payment facilitation, even as that business becomes commoditized. Merchants are witnessing the transformation of the point of sale. Formerly a simple transaction utility, it is now just one step in a process of engaging customers digitally, leveraging data to improve customer engagement before, during, and after the transaction. There is a clear opportunity for payment providers that can expand beyond their traditional scope of service and collaborate more effectively with merchants to use data in order to create richer and more personalized shopping experiences.

To capture this opportunity, merchants and payment providers will need to focus on four priorities: (1) improve customer engagement and loyalty; (2) develop a better understanding of customer data; (3) integrate data among channels more effectively; and (4) ensure high levels of security.

A digital revolution in retail shopping

The most fundamental shift facing retailers is the digitization of commerce. Over the past 30 years, consumers have shifted their payment method from cash and checks to credit and debit cards. It is estimated that cash and checks will be used for just 15 percent of total personal spending in the U.S. in 2018, down from 30 percent in 2013, with credit cards, debit cards, and other electronic payment methods making up the remaining 85 percent.1 Though this shift to electronic payments was evolutionary, the expansion from digital payments to digital commerce — in which a consumer engages digitally before, during, and after a retail transaction — has been revolutionary.

The most fundamental shift facing retailers is the digitization of commerce.

The rapid and broad adoption of digital commerce is forcing merchants to adapt and adjust. Merchants are well aware of the opportunities they can derive from digital shopping technology, but the shift to digital commerce also brings new challenges that they may not yet be equipped to handle. These challenges include more consumer touch points in an increasingly omnichannel shopping environment; more data-generated insight on consumer shopping behavior; more communication options to engage with the consumer; and more privacy and security concerns. Similarly, payment providers have been caught flat-footed by the shift to digital commerce — they still focus too much on payment facilitation, which has become a commodity.

The Strategy& 2015 Consumer Payments Survey, conducted with the Electronic Transactions Association (a consortium of payment providers, technology vendors, and others in the payments ecosystem), analyzes the impact of this shift on both merchants and payment providers. To conduct the survey, we contacted consumers, merchants, and payments executives to assess their attitudes on payment trends. The results indicate a clear shift in consumer behavior thanks to the digitization of commerce — that is, the ability for consumers to shop anywhere, anytime, whether using a home computer or a mobile device.

Keeping three kinds of consumers happy

The consumer shopping experience has undergone historic changes in the last few years. A 2014 report by Forrester Research estimates that online sales will increase from US$294 billion in 2014 to $414 billion in 2018. During that same period, offline sales are projected to decrease. Even more telling, consumers are increasingly using digital tools to shop. Forrester estimates that Web-influenced offline sales will increase by $392 billion. That’s a shift for e-commerce — online and Web-influenced offline sales combined — from about 52 percent of total sales in 2014 to 59 percent in 2018, meaning that it is growing in both absolute terms and as a percentage of all retail sales.2

Consumers are increasingly using digital tools to shop.

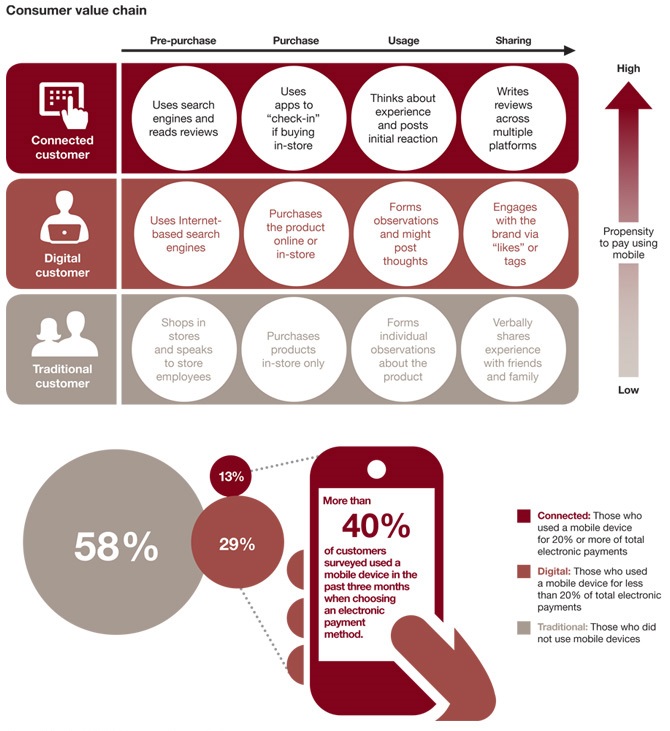

Despite this significant growth in digital and mobile shopping, many customers still do not use digital tools when they shop. To understand the differences among customers, we asked consumer respondents to indicate an approximate percentage of their total electronic payments — whether using a credit card, a service such as PayPal, or a mobile wallet or app — over the past three months. Using this categorization — particularly the mobile percentage — we were able to define three consumer profiles (see Exhibit 1):

- Connected: Those who used a mobile device for 20 percent or more of total electronic payments over the past three months

- Digital: Those who used a mobile device for less than 20 percent of total electronic payments over the past three months

- Traditional: Those who did not use mobile devices over the past three months

Exhibit 1: Three consumer profiles — connected, digital, and traditional — each have different shopping habits and needs along the value chain

Several distinctions among these three groups were immediately apparent from the survey results. For example, traditional customers highly value savings and security; fear of potential vulnerability from digital makes them hesitant to use mobile devices. Conversely, connected and digital customers are aware of the perceived security risks but value convenience and saving time enough that they’re willing to set aside any concerns they might have.

The disparate groups present a challenge for merchants, which must satisfy the more than 40 percent of consumers who use digital tools to shop — across multiple channels — while still accommodating non-digital, traditional customers.

Another challenge for merchants is that they must navigate a more complex payment environment, with multiple, confusing options from a range of players including technology giants like Apple and Google as well as startups like Square. The survey findings indicate that overall customer satisfaction with digital payments is mixed. Customers are satisfied with the convenience of digital payments, and they appreciate the fact that merchants accept multiple payment solutions. Yet there is considerable room for improvement in areas such as privacy, rewards and savings, and security (see Exhibit 2).

Complexity remains a challenge

Omnichannel shopping, expanding payment options, and increased security concerns are creating a significant amount of operational complexity for merchants. The survey results indicate that merchants are well aware of this issue. When asked to identify the most important industry trends, they focused on shifts in the digital technology space (see Exhibit 3). The shift to mobile technology was important (cited among the top three trends by 50 percent of respondents), but the merchants also identified a more notable change that comes with digital: a shift to a consumer shopping experience with embedded payment, cited in the top three by 67 percent. Another major trend was the security of payment and personal data in transit across wireless technology, in point-of-sale devices, and in back-end databases.

Merchants are also split when it comes to identifying the best strategy for digital payments and mobile wallets.

Their mobile wallet strategies vary widely (see Exhibit 4). Some 38 percent of merchants responding to the survey either have joined or plan to join an open-branded wallet program, such as those offered by Apple, Google, and Samsung. Another 19 percent have joined or plan to join an industry mobile wallet program, such as CurrentC, and 12 percent are considering internally branded solutions, such as those deployed by Starbucks and Subway. Notably, 25 percent currently have no strategy regarding mobile wallets.

Exhibit 4: Merchant enterprises’ mobile wallet strategies vary widely

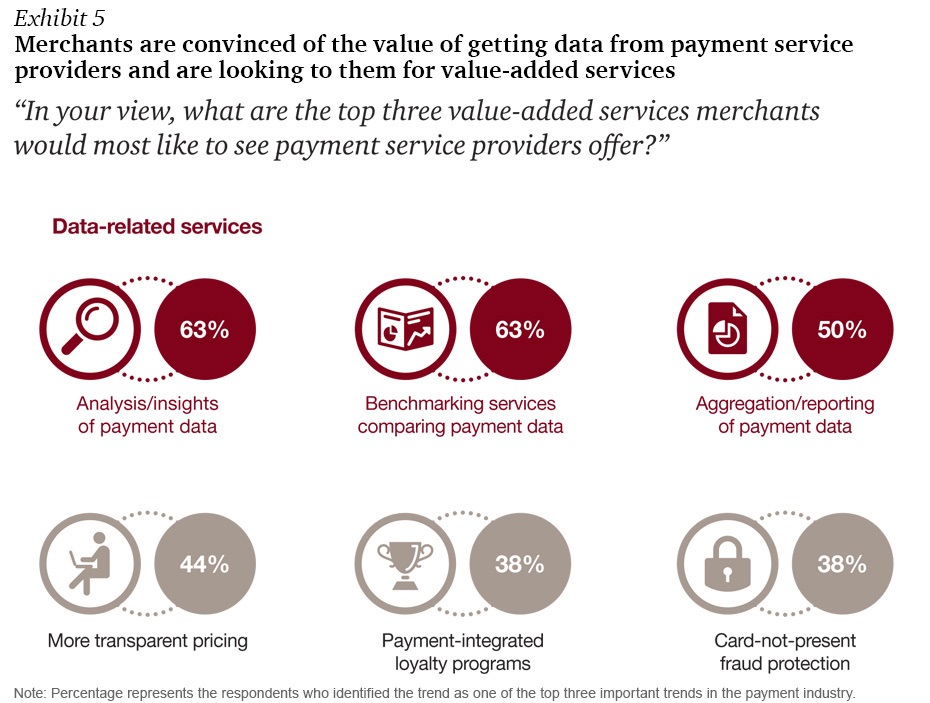

One area of clear consensus among merchants is the value-added services they would like to see from payment providers: meaningful insight into customer behavior and the ability to use that data to increase customer engagement and loyalty. When merchants were asked what value-added services they’d most like to see from payment service providers in this regard, the top three responses were all related to data — analysis and insights of payment data, benchmarking services comparing payment data, and aggregation and reporting of payment data (see Exhibit 5).

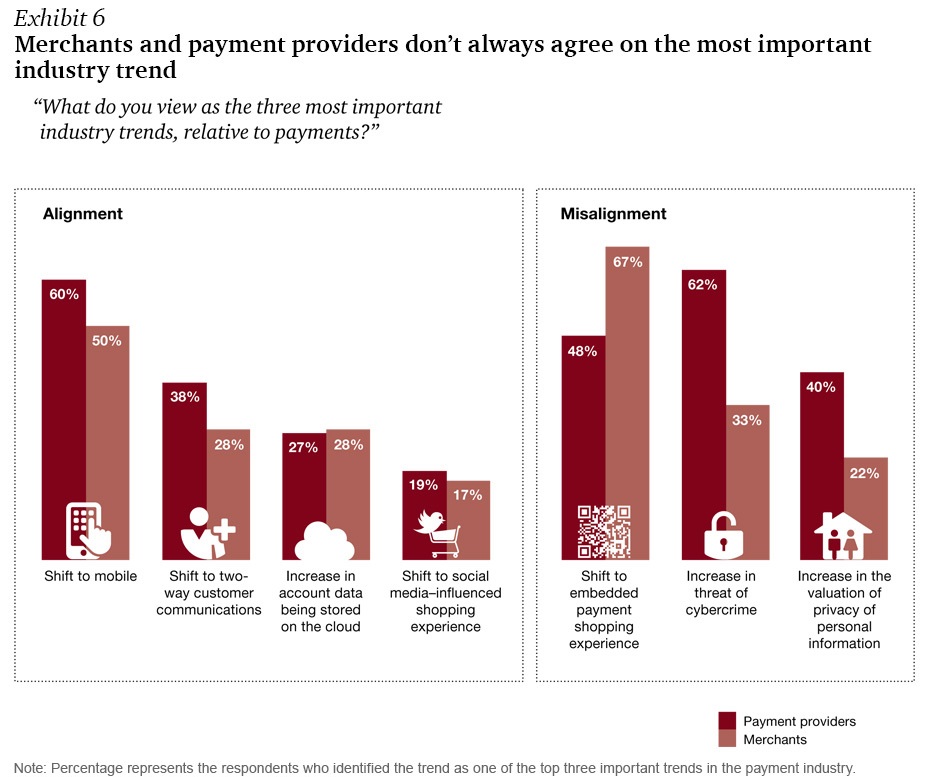

A critical finding is that the key trends identified by payment provider respondents differed from those identified by merchants. Certainly, on some issues, the two groups concur. For example, they both identified the shift from static, one-way customer engagement to tailored, two-way communication as a key trend.

Yet there were large differences in areas such as valuing personal privacy and protecting against cybercrime, cited among the top three trends by a larger percentage of providers than merchants. The biggest difference, however, came in perceptions of the consumer experience. When asked about the shift from a consumer payment experience to a consumer shopping experience, only 48 percent of payment providers found it important, compared with 67 percent of the merchant respondents (see Exhibit 6).

Clearly, payment providers need to focus on the areas of misalignment to improve their relationships with merchants. Though many payment providers are still focused primarily on facilitating payments (including security), consumers and merchants consider those aspects to be fundamental, and merchants want more data-driven, value-added services. To meet this demand, payment providers need to partner more proactively with merchants in improving the entire customer experience — both before and after the payment transaction.

A holistic view of customers

Simply put, merchants need to understand more than what happens at the point of purchase. They need to use data to piece together an end-to-end view of the shopping experience. Payment providers can leverage their data in this way and help merchants develop a holistic view of their customers.

For instance, in leveraging pre-purchase data, payment providers can help merchants determine how effective their marketing campaigns are, by identifying direct attribution of digital and traditional marketing efforts that drove actual, incremental sales. For example, did consumers respond to a text advertisement because they were in the neighborhood, or had the consumer already been exploring the merchant’s website?

When it comes to data derived from the payment transaction itself, payment providers can help merchants in several areas, including payment and rewards systems, security and fraud monitoring, simplified checkout, and real-time settlement options.

Merchants need to understand more than what happens at the point of purchase.

And with post-purchase usage data, payment providers can help merchants track participation in loyalty programs, as well as aggregate consumer information to analyze behavioral and demographic data. From a security perspective, the ability to track fraud data is also important.

With this kind of insight from all three phases of the shopping experience, merchants can create a more detailed view of their customer base. At that point, they can use the ensuing data to increase service, efficiency, and engagement, through a virtuous circle that helps them become smarter and more efficient. Some of these factors are fundamental, while others will allow merchants to differentiate themselves from the competition. The ultimate goal: to create the best customer experience possible, increase customer loyalty, and avoid commoditization.

The problem of stored credentials

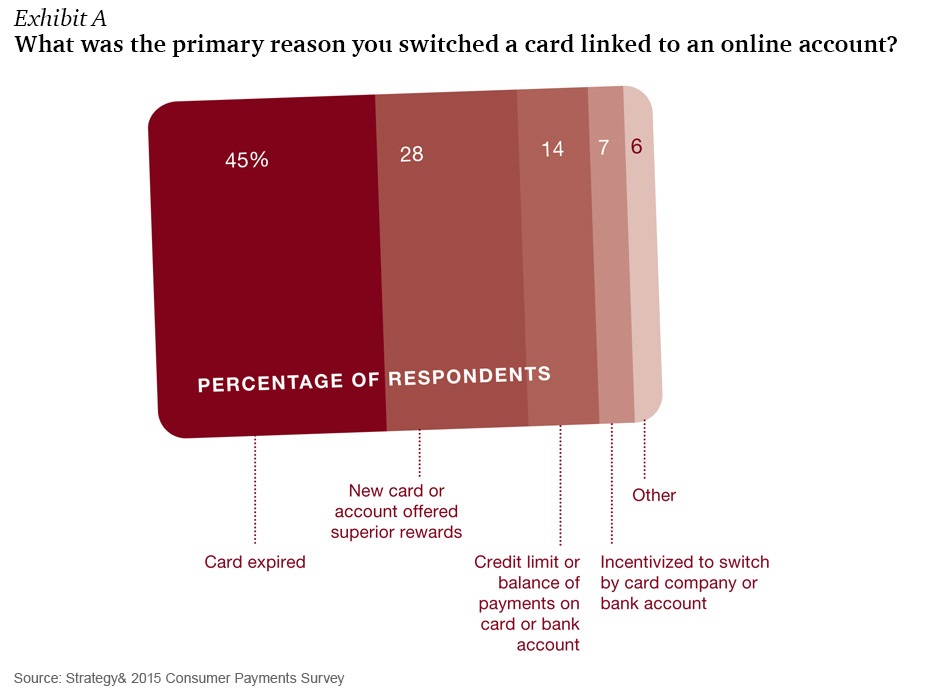

Keeping card credentials current in card-linked loyalty programs is becoming a key challenge for both merchants and payment providers. According to our research, the primary reason that consumers switch a card linked to online accounts — far more than any other reason — is that the card expired (see Exhibit A)

Similarly, a growing number of consumers are making purchases through their mobile devices, mostly through app purchases using stored credentials, such as the one-click “buy now” buttons on Pinterest or Google Search.

One potential solution is tokenization, in which programs link to proxy data such as an email address and password (the token) rather than to the underlying card data. Since more data can be securely passed with every tokenized transaction — compared with today’s non-tokenized transactions — token providers will soon be able to easily identify when cards are expiring soon and facilitate the process of helping consumers update them. In this way, merchants will soon be able to address the single biggest factor behind switching cards.

Four recommendations: How merchants and payment providers can move forward

With an awareness of both the challenges and the potential payoffs highlighted in the survey results, we believe that the next step for merchants and payment providers alike should be to focus on four priorities:

Improve customer engagement and loyalty. Merchants and their payment providers must view payments as an opportunity to engage with customers, not just an area of cost or additional complexity. Payments are no longer a discrete act, but rather one part of a process that begins with marketing and continues with personalized efforts to cement customer loyalty after a purchase.

Develop a deeper and broader understanding of customer data. Capturing, synthesizing, and packaging data will be essential to improving customer loyalty. Merchants and payment providers can use this data on both an individual and an aggregate level, in order to develop more detailed insights into specific consumers and larger demographic groups.

Integrate data among channels more effectively. Merchants and payment providers must build systems that can easily share data, both internally among departments and externally among partners. By building systems with flexible architectures, merchants can improve their ability to integrate data from different sources.

Ensure high levels of security. Merchants and payment providers will have to work together on data security, given its status as a top concern among customers. That means ensuring they’re ready to accommodate new security mandates, such as the EMV chip-and-pin technology, and deploying end-to-end encryption to protect consumer data and financial information. The stakes are too high — merchants that don’t get security right will lose customers.

These recommendations are interrelated. To be truly successful, and to create a foundation for success long into the future, merchants and payment providers need to collaborate on all four, and build the right foundation to capitalize on the looming growth in digital payments. The digital payment journey may be arduous, but the payoff, in terms of enhanced customer engagement and loyalty, will be worth it.